Summary

- In 2025, the six-month T-bill's cut-off yield dropped to its lowest point of the year at 1.44%.

- This decline is attributed to low global interest rates, strong demand for T-bills, decreasing inflation in Singapore, and MAS issuance management.

- BigFundr Deals outperform T-Bills in yield, liquidity and fees.

If you have been considering investing in Singapore Treasury Bills—also known as T-Bills—you may want to re-evaluate how this will impact your finances.

The latest six-month T-bill closed with a cut-off yield of 1.44%, lower than the 1.59% seen at the previous auction on 14 August 2025. This is the lowest yield so far in 2025 and the 12th straight drop since March. The median yield came in at 1.39% (down from 1.55%), while the average yield was 1.3% (down from 1.48%).

A yield refers to your earnings in interest.

What is a Singapore Treasury Bill?

A T-Bill is a short-term, low-risk government security issued by the Monetary Authority of Singapore (MAS), usually issued in 6 or 12-month terms.

T-bills are sold at a discount to their face value. When it matures, i.e. reaches its full term, the Singapore Government pays back the full face value. The difference is the interest you earn.

Why have T-Bills fallen so low?

Source: Monetary Authority of Singapore

Global interest rates are expected to stay low

Singapore doesn’t set interest rates like most countries; instead, it follows global interest rate trends, especially the US Federal Reserve (Fed). As the Fed is expected to cut rates or keep them lower for longer, demand for short-term government debt has pushed yields down.

Strong demand

Growing demand for T-bills has been pushing prices up, and hence, yields decrease. Demand can come from retail investors, local and international institutions such as banks and wealth management firms, and international investors.

Inflation outlook

Singapore’s inflation has been coming down over the past years—our headline inflation rate is now at a 4-year low at 0.8%. As inflation comes down, investors are more willing to accept lower returns for the safety of government securities.

MAS issuance

The government manages how much debt is issued to meet its needs. If the government issues fewer T-Bills against a strong demand, the yields will drop.

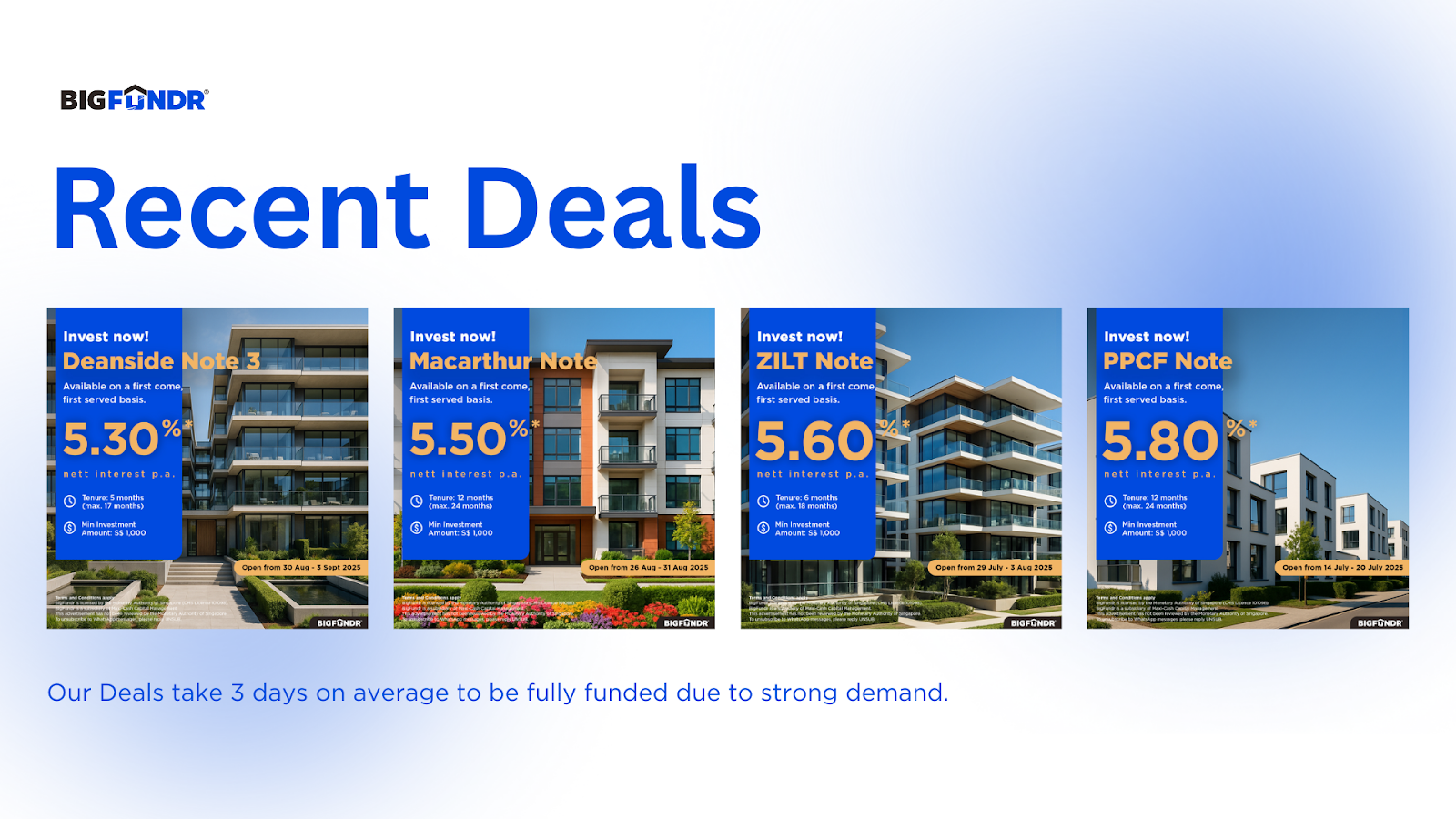

BigFundr Deals VS T-Bills

Note: Figures accurate as of 19/09/2025

Why BigFundr Rates Are More Resilient In Periods of Low Interest Rates

Founded in 2019, BigFundr is Singapore’s premier MAS-licensed investment platform (CMS Licence No. 101098) delivering attractive, risk-adjusted investment returns through fixed income instruments secured by low-risk property assets. To date, we have returned 100% of all investor capital at above-market interest earnings paid monthly with 0 defaults or delays—a track record that consistently beats industry benchmarks in Singapore and worldwide.

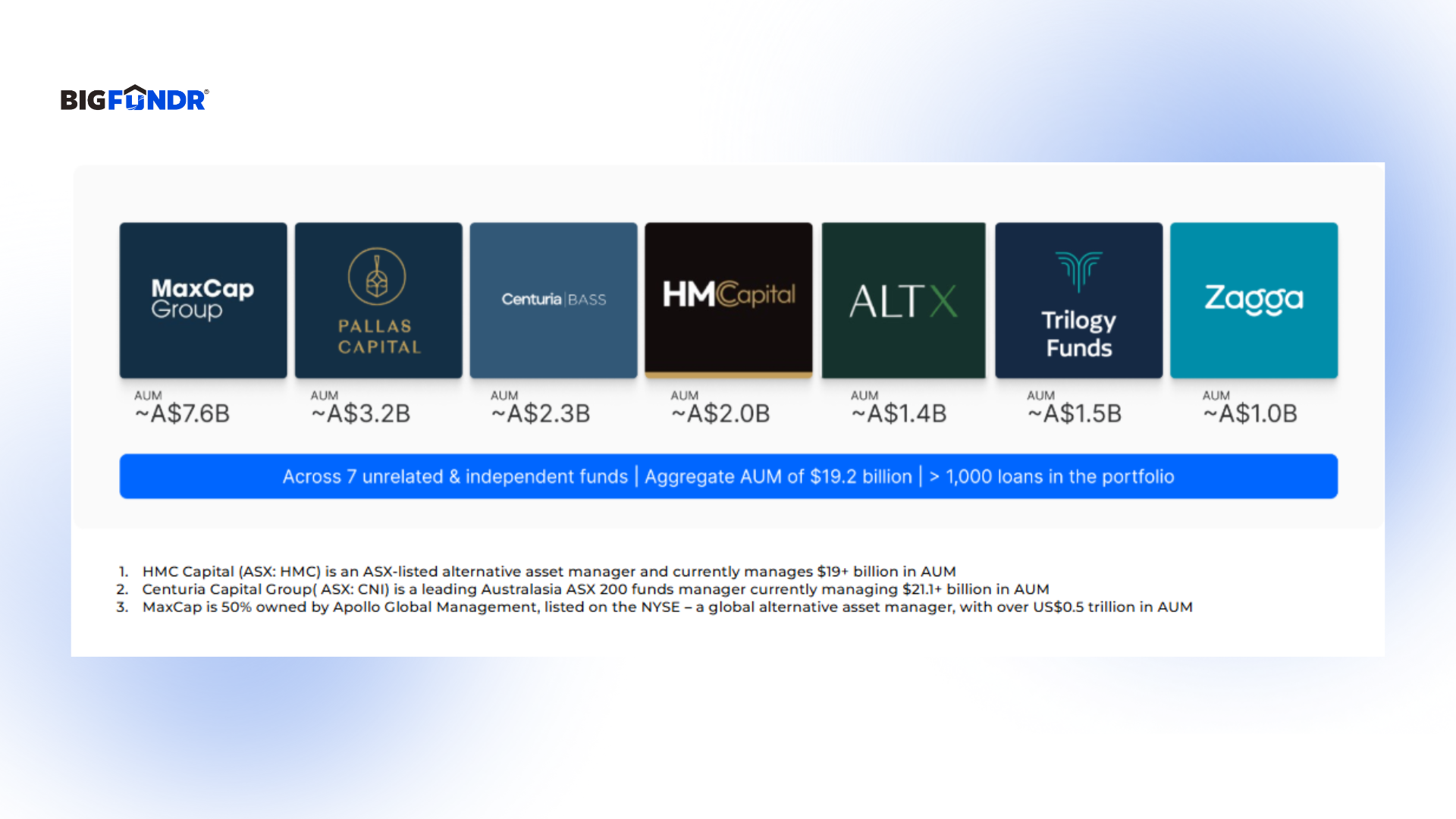

Our investment opportunities are structured to deliver strong returns over flexible terms thanks to our network of licensed trustees, well-established fund managers, and developers with solid track records. We partner exclusively with top fund management firms in Australia, each managing more than A$1 billion in AUM, to structure property development Deals with defined rates of return, tenures, and rigorous credit assessment and due diligence.

With decades of experience in the finance and real estate sectors, and a deep network of industry partners with solid track records, we provide investors access to Deals that deliver enhanced returns that outperform the market—up to 5.50% for SGD and 7.00% for AUD and USD nett (rates are as of 16/09/2025).

Our combination of fixed rates, collateral, and a strong background in structuring low-risk, high-quality investments helps keep returns higher than market even when interest rates fall, providing investors an alternative to other fixed income instruments such as T-Bills.

Are T-Bills and BigFundr Deals Suitable For You?

The Singapore T-Bill is a good instrument if you want a safe and low-risk place to park your money without having to lock it up for too long. However, its yields are modest compared to other alternatives, and you will only receive payment at maturity.

Consider investing some of your savings in BigFundr Deals, starting from a low minimum of S$1,000, to earn up to 5.50% nett interest p.a. and enjoy relatively good liquidity with short 6 to 12-month terms with interest paid monthly. Investors can rest assured that their investments are backed by low-risk, high-quality property developments and protected by multiple layers of safeguards. Open a BigFundr account today!

Investing 101 with BigFundr

Stay ahead of the curve with our latest articles and insights about investing.

.png)